The Appraisal Blog

The Value of Impact of Flood Zones

The Value Impact of Flood Zones

Few things can surprise buyers more than discovering a home that sits in a flood zone that requires additional insurance. From an appraisal standpoint, being in a flood zone often reduces market value.

The impact varies: sometimes it’s the direct cost of flood insurance, sometimes it’s just the stigma of risk. I measure it by comparing sales inside vs. outside the zone. If buyers consistently pay less for otherwise similar homes in a flood zone, that difference becomes the adjustment.

Agents can help by clarifying flood insurance costs early and making sure it’s disclosed. A buyer who knows up front will be less shocked if the appraisal makes an adjustment.

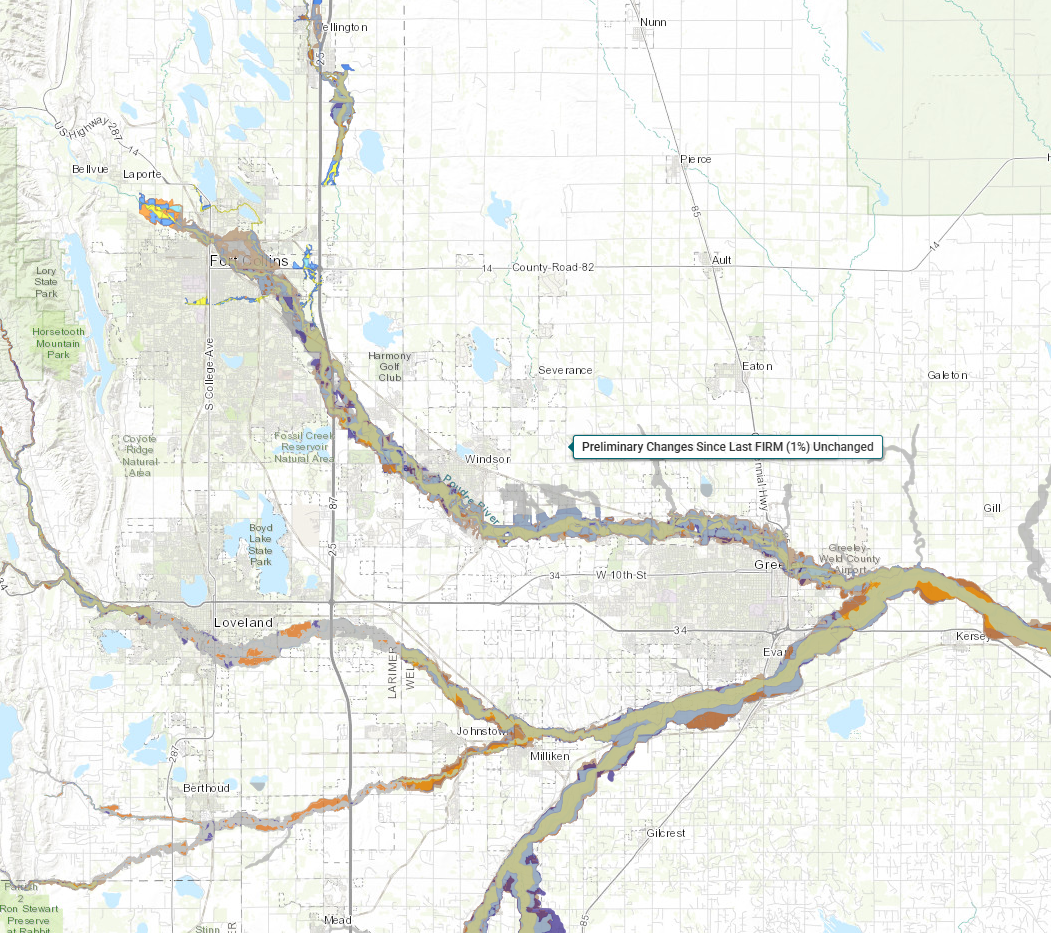

Flood Map with Preliminary Changes Since Last FIRM 1%

https://coloradohazardmapping.com/map

Legend

Orange: Increase

Purple: Decrease

Gray: Unchanged

Measuring Homes: ANSI Standards Matter

Measuring Homes: ANSI Standards Matter

Measuring Homes: ANSI Standards Matter

One of the biggest sources of confusion between agents and appraisers is how a home is measured. Since 2022, Fannie Mae requires appraisers to follow ANSI standards for measuring and reporting Gross Living Area (GLA).

The key point: only fully above-grade finished space counts as GLA.

This means a basement, even if fully finished, is not added to the total GLA. It’s reported separately. A 2,000 sqft home with a 1,000 sqft finished basement is not treated as a 3,000 sqft home in the appraisal. Basement space still has contributory value, but usually at a lower rate per square foot.

This is why MLS data and county records often conflict with appraisal reports especially in split-levels with garden levels. If MLS shows 3,000 sqft by including basement space, but ANSI requires 2,000 sqft GLA with 1,000 sqft basement, that difference can frustrate buyers and agents.

My advice: always clarify to clients how square footage is being reported to avoid surprises.

Solar Panels and Contributory Value

Solar Panels and Contributory Value

Solar panels are a common conversation starter, but from an appraisal standpoint, they aren’t simple.

The first step is ownership: leased systems are personal property, not real estate, and don’t add value. Panels with consumer debt are also considered personal property and given not value since they may be foreclosed on and removed. Owned systems are considered real property, but even then, the market reaction varies.

When analyzing contributory value, I look for paired sales in the neighborhood – homes with and without solar, matched for size and condition. I also use pvvalue.com which can help with the income and cost approaches for solar panels.

Effective Age vs Actual Age

Effective Age vs Actual Age

We all know the “year built” on a property, but in appraisal, we also consider effective age. A home built in 1980 may “feel” like a 2005 property if it’s been fully remodeled. On the flip side, a 10-year-old home with no maintenance could appear like a 25-year-old one.

Effective age impacts depreciation and the cost approach, but more importantly, it reflects how buyers perceive condition. If updates lower the effective age, the home will likely compete with newer comps in the market. I analyze not only the updates completed, but also the quality and how recently they were done.

For agents: when marketing a property, be specific about the updates and their timing. “Kitchen remodeled in 2022 with quartz counters and new cabinetry” will often help me justify a lower effective age in the report, which can positively impact value.

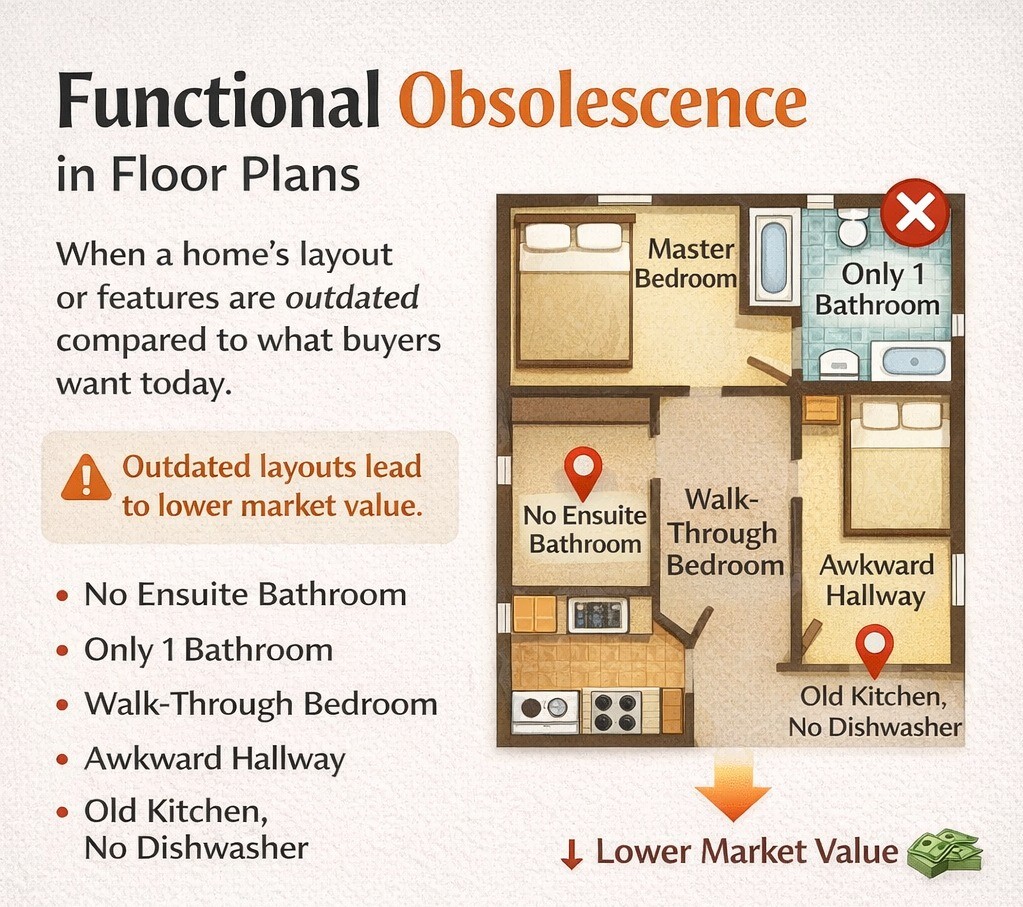

Functional Obsolescence in Floor Plans

Functional Obsolescence in Floor Plans

Functional obsolescence is one of the trickier things we run into as appraisers, and it can take many forms. A common example is when you have to walk through one bedroom to get to another, or when a home has only one bathroom serving four bedrooms. Buyers notice these things, and the market often discounts them.

When I appraise a home with a functional flaw, I start by looking for other sales with similar layouts to see how buyers reacted. Did they sell for less than other homes of similar size and condition? If so, that discount gives me an idea of the adjustment. If I can’t find a perfect match, I’ll weigh buyer preferences and sometimes even consult builders for cost-to-cure estimates.

The important takeaway: just because a home is large or updated doesn’t mean the market will overlook awkward layouts. Agents can help buyers and sellers understand that design matters, and appraisers must measure the actual impact on value.

Contributory Value of an Outbuilding

Contributory Value of an Outbuilding

Valuing an outbuilding can be difficult. First thing I determine is if the building is permanently attached to the lot, if not and be removed it is personal property, not real property. I usually go one of two routes when valuing the barn, shop or shed while developing my appraisal.

I complete the cost approach to the outbuilding and apply depreciation to get the depreciated cost of the outbuilding. I use cost data from the National Building Cost manual.

I also determine how many vehicles the outbuilding can hold. It takes about a 10’x20’ space for each vehicle.

Using comparable sales, I determine if the market accepts and gives value to the outbuilding. If so, I will reconcile the two values for an adjustment to apply to the comparable sales.

If you run into trouble placing value on an outbuilding, please send a message or post here and we can kick it around!

Split-Level Homes – Adjusting for Style

Split-Level Homes – Adjusting for Style

As you know, ranches tend to sell for more than a similar sized 2-story and 2-stories tend to sell for more than a similar sized split level.

When I am valuing a split level, I typical search for non-ranch style homes similar in total square feet. The reason I use total square feet when searching the MLS is that not all listing agents treat the size of split-levels the same.

Appraisers have to follow ANSI standards which require any below grade area as a basement. It is best to compare the same style, but in some cases due to lack of data we have to compare homes of different style.

If the most likely substitutes for the subject property includes properties that differs in style, I would search for sales to pairs to compare to determine a market reaction, if any, for the different style.

If you are listing a split-level, in an area of primarily ranches and two-stories and struggling with any market reaction, please give me a call and we can tackle it together.

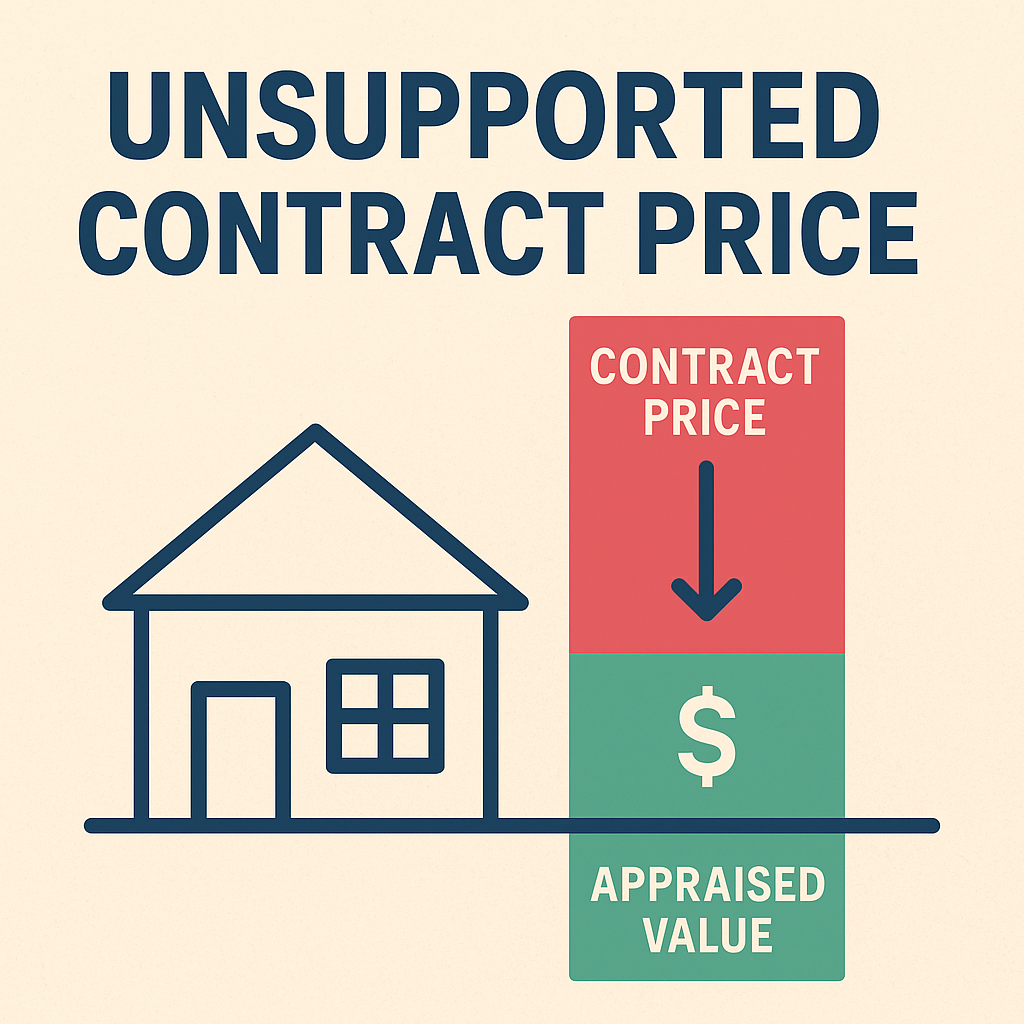

Unsupported Contract Price

Unsupported Contract Price

It does not happen often, but occasionally I am unable to support the contract price for an appraisal for lending purposes.

When I am unable to support the contract price with data, I contact the listing agent and request the sales used to price the property. Perhaps something did not show up in my search for comparable sales. Perhaps the agent knew of a sale that was not in MLS or a listing had a data entry error resulting in it not showing up on the search.

I welcome agents sharing the sales used to price their listings. Typically, we are using the same sales, but if the agent has some, I did not originally consider, I will consider them.

I can’t speak for all appraisers, but not supporting the contract price brings no joy and takes longer to complete the appraisal.

Overimproved for the Neighborhood? Here’s How That’s Handled

Overimproved for the Neighborhood? Here’s How That’s Handled

Ever listed a home with a unique feature or upgrades far beyond anything else nearby?

Appraisers refer to this as superadequacy or over-improvement and yes, it matters.

We typically determine whether the market supports the premium features. For example:

Marketability – Are there sales in the neighborhood (or in a competing area) that include a similar feature or over-improvement? Without comparable sales, we can’t demonstrate market support or justify an adjustment for the premium feature.

Cost does not equal value – Just because something was expensive to install doesn’t mean the market will pay for it.

Have you come across any great examples of over-improvements? Was your client able to recover the cost?

If you’re listing something unique, I’m happy to review comps or discuss how value might be reconciled in today’s market.

Divi Real Estate

There are many variations of passages of Lorem Ipsum available, but the majority have suffered alteration in some form, by injected humour

Contact

(923)-234-6788

Offices

4254 Divi St. San Francisco, CA

2354 Extra Blvd. San Jose, CA